Welcome to the world of big-league real estate! If you’re reading this, you’ve likely already dipped your toes into the residential rental market. Maybe you own a few single-family homes or a duplex, and you’re starting to realize that managing ten different houses in ten different locations is a logistical headache. You’re ready to scale, and that means looking at properties with multi family 5 units or more.

But here’s the catch: once you hit that fifth unit, the rules of the game change entirely. You aren't just buying a bigger house; you're buying a business. At Emerald Capital Funding, we see investors make this jump every day, and while it feels like a giant leap, we’ve got you covered. This guide will equip you with everything you need to transition from residential thinking to mastering commercial loans.

Why the Number Five Changes Everything

In the eyes of the lending world, there is a massive wall between a four-unit property and a five-unit property. Anything with one to four units is considered "residential." You can often snag these with a 30-year fixed mortgage, lower down payments, and loans backed by Fannie Mae or Freddie Mac.

Once you add that fifth unit, you cross over into the realm of commercial real estate. Why does this matter? Because commercial loans are structured differently, priced differently, and evaluated differently. You’re no longer being judged solely on your personal salary as a software engineer or a nurse; you’re being judged on how well that building can "work" for a living.

The Big Mindset Shift: It’s About the Property’s Paycheck

If you’ve bought a home before, you know the drill: the lender wants your W-2s, your tax returns, and a deep look at your personal Debt-to-Income (DTI) ratio. They want to know if you make enough money to pay the mortgage.

When you move into multi family 5 units or more, the focus shifts from you to the building. This is often referred to as a "DSCR-ish" approach, but on a much larger scale. Lenders care about the Net Operating Income (NOI). They ask: "After paying for water, taxes, insurance, and the super, is there enough money left over to pay the bank?"

Actionable Takeaway: Focus on the T12

Before you even talk to a lender, ask the seller for the "T12": the trailing 12 months of profit and loss. This is the property’s resume. If the T12 shows consistent income and managed expenses, your path to a commercial loan becomes much smoother.

Understanding the Numbers: LTV vs. LTC

In the residential world, you might be used to putting 3.5% or 5% down. In commercial lending, you’ll need to bring a bit more "skin to the game." Generally, you should expect to contribute approximately 25% of the property's value as a down payment.

Lenders look at two main ratios:

- Loan-to-Value (LTV): This is the percentage of the property’s current appraised value the bank will lend. For a solid multi-family deal, you’re usually looking at 75% to 80% LTV.

- Loan-to-Cost (LTC): If you are buying a "fixer-upper" apartment complex, the lender looks at the total project cost (purchase price + renovation budget). We often provide up to 90% LTC financing to help investors keep their cash liquid for other deals.

Success is within your reach if you plan for these capital requirements early. You can check out our services page to see how we structure these different ratios.

What Commercial Lenders Are Actually Looking For

Don’t worry; you don't need to be a billionaire to get a commercial loan, but you do need to show "Sponsor Strength." While the building’s income is the star of the show, the lender still needs to know who is behind the curtain.

- Credit Score: Usually, a 650 or higher is the baseline.

- Liquidity: Lenders want to see that you have "post-closing liquidity." They don't want you to spend your last dollar on the down payment. They like to see that you have enough cash in the bank to cover 6-12 months of mortgage payments just in case of emergencies.

- Experience: If this is your first 10-unit building, a lender might want to see that you’ve managed smaller rentals before or that you’ve hired a professional property management company.

The Documentation Deep Dive

One of the biggest hurdles for beginners is the sheer amount of paperwork. Commercial underwriting is thorough. To stay ahead of the game, start gathering these documents now:

- The Rent Roll: A list of every unit, who lives there, how much they pay, and when their lease ends.

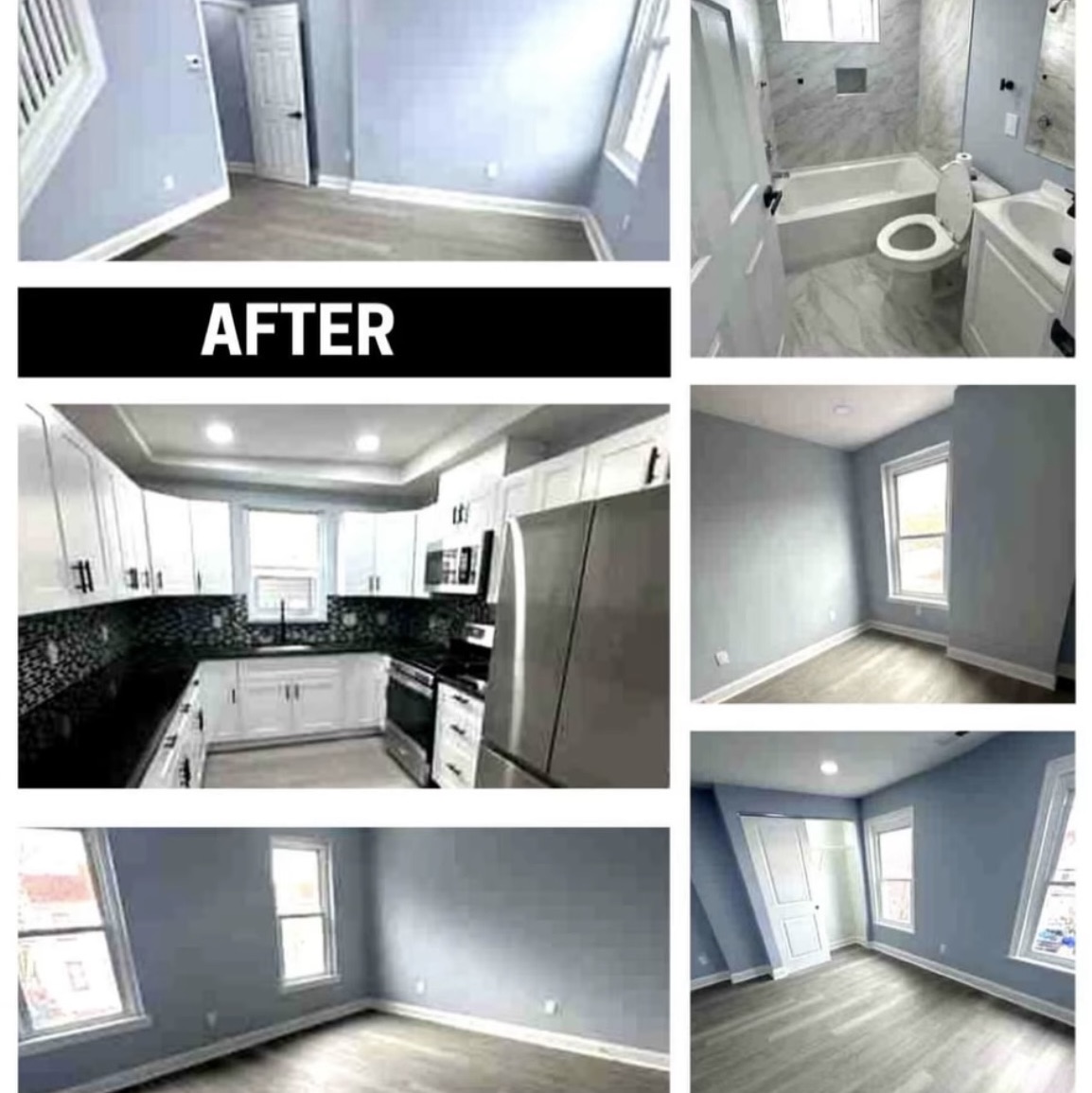

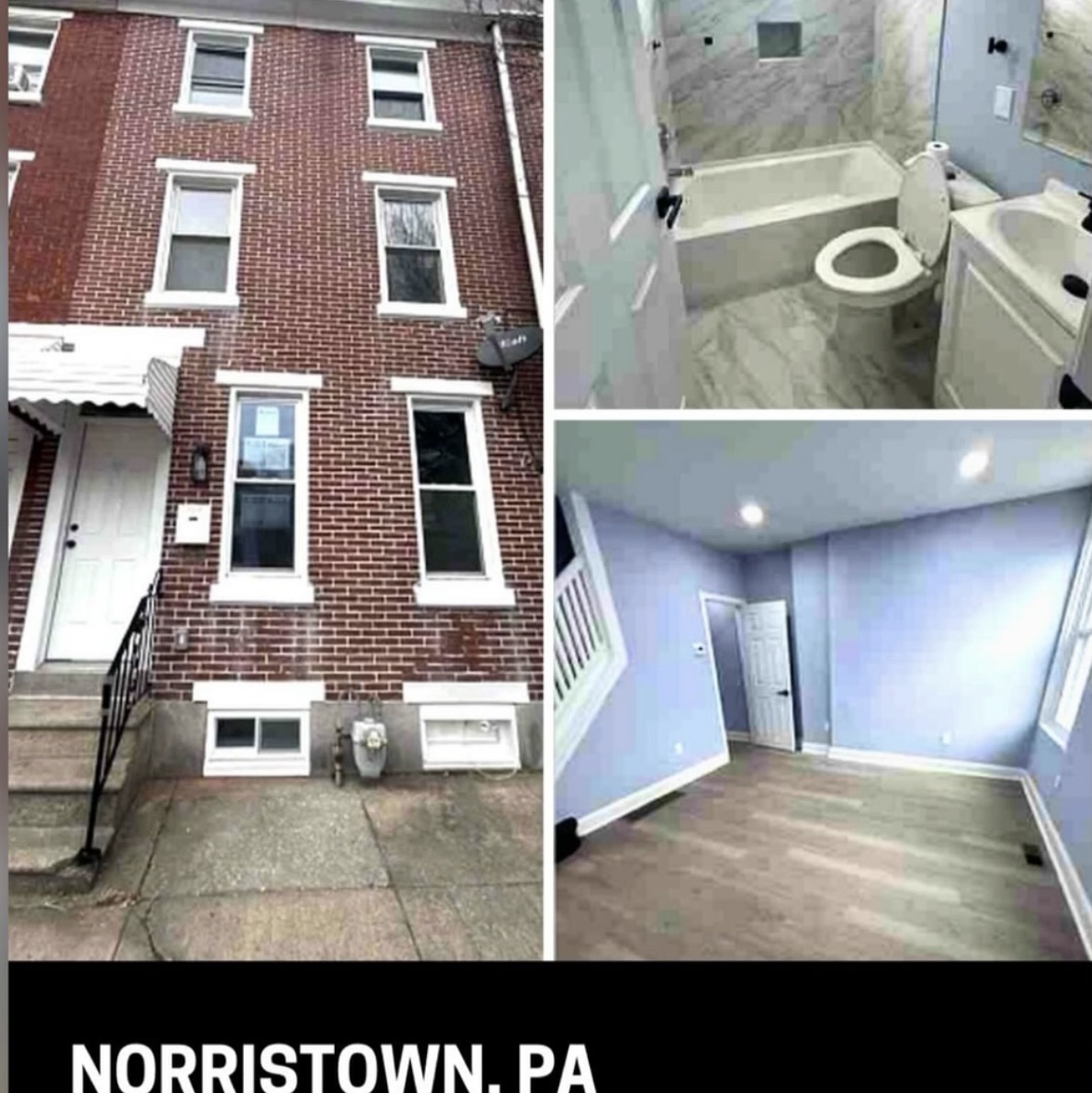

- Property Photos: High-quality images of the exterior, common areas, and at least a few unit interiors.

- The Offering Memorandum (OM): If you’re buying through a broker, they’ll provide this. It’s basically a marketing package for the property.

- Schedule of Real Estate Owned (SREO): A spreadsheet of every other property you own and how they are performing.

Having these ready when you apply now will set you apart as a professional investor rather than a hobbyist.

Choosing the Right Loan for Your Strategy

Not all commercial loans are created equal. Your choice depends on your "exit strategy."

- Permanent Loans: These are for the "buy and hold" investor. They usually have terms of 5, 7, or 10 years with a 25- or 30-year amortization schedule.

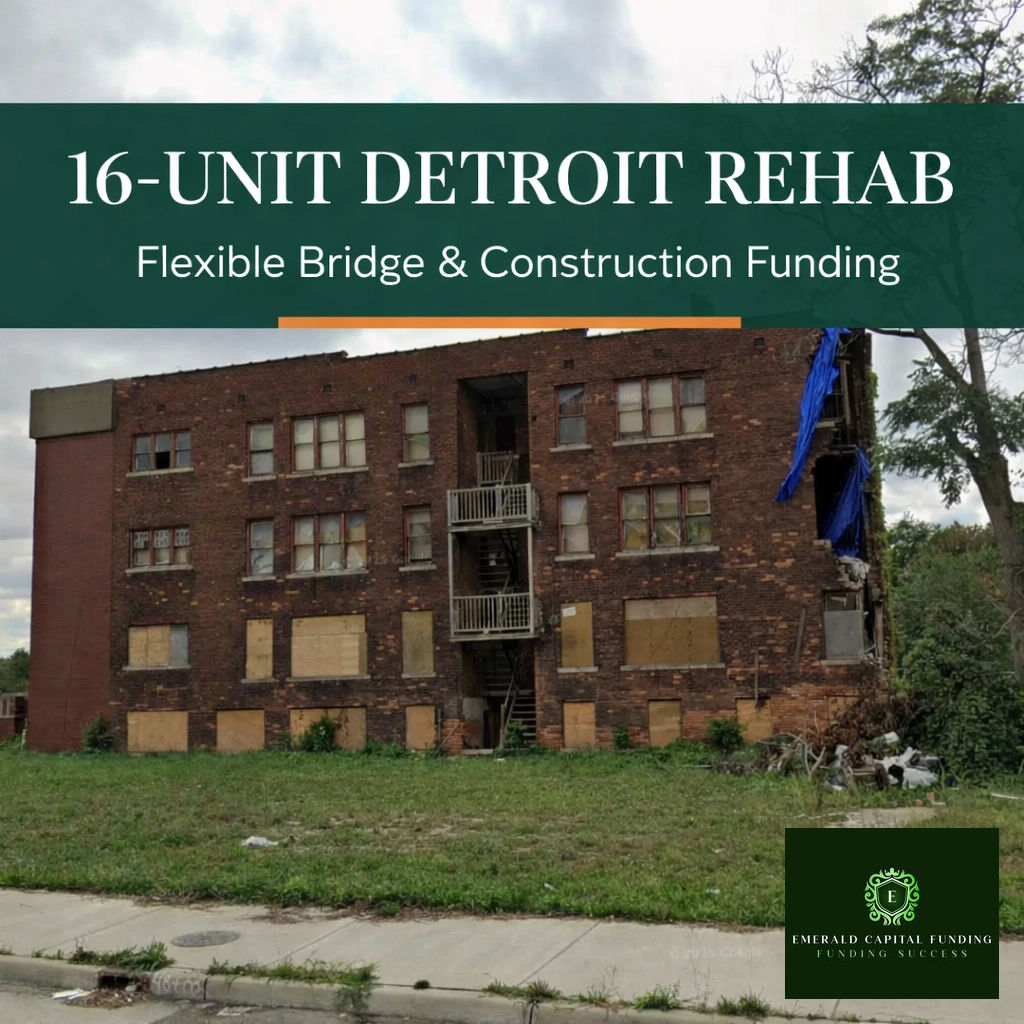

- Bridge Loans/Hard Money: If the building is currently empty or needs major repairs, a traditional bank won't touch it. You’ll need a bridge loan to buy it and fix it up before "refinancing out" into a permanent loan.

- Agency Loans (Fannie/Freddie): These offer the best rates but have very strict requirements regarding the property’s condition and your own net worth.

Actionable Takeaway: Know Your Timeline

If you plan to flip the building in two years, don't get locked into a 10-year loan with a heavy prepayment penalty. Always match your financing to your business plan.

Common Pitfalls to Avoid

Scaling to multi family 5 units or more is an exciting pathway to financial security, but watch out for these rookie mistakes:

- Underestimating Expenses: In residential, you might just think about taxes and insurance. In commercial, you have to account for vacancy rates (usually 5%), property management fees (8-10%), and "CAPEX" (saving for that roof that will eventually leak).

- Ignoring Zoning: Just because a building has five doors doesn't mean it’s legally zoned for five units. Always verify the Certificate of Occupancy.

- Going It Alone: Commercial real estate is a team sport. You need a good lender, a solid contractor, and a sharp accountant.

Q&A: Common Questions for Commercial Beginners

Q: Can I use a commercial loan to buy a property I want to live in?

A: Generally, no. Commercial loans are for investment properties. If you plan to "house hack" a 5-unit building, you might still qualify for certain programs, but the underwriting will still focus on the business aspect of the property.

Q: Is the interest rate higher than a home loan?

A: Often, yes. Because commercial loans are considered higher risk for the bank, the rates are typically 0.5% to 2% higher than a standard 30-year residential mortgage. However, the tax benefits and cash flow of a larger building usually more than make up for the difference.

Q: How long does it take to close?

A: While a home loan can close in 30 days, commercial deals usually take 45 to 60 days. There are more "moving parts," like environmental reports and commercial appraisals.

Your Pathway to Scaling

Moving into the 5-unit+ space is how real wealth is built in this industry. It allows you to use "economies of scale": fixing one roof over ten tenants is much cheaper than fixing ten roofs over ten tenants.

At Emerald Capital Funding, we specialize in helping investors bridge that gap. Whether you're looking for your first 5-unit apartment or you're looking to sell an auto loan portfolio to gain more liquidity, we’re here to help you navigate the complexities of the commercial market.

With the right approach and a solid team behind you, mastering commercial loans is entirely within your reach. Ready to see what your numbers look like?

Contact us today or jump straight into the process by visiting our application page. Let’s get your next deal funded!